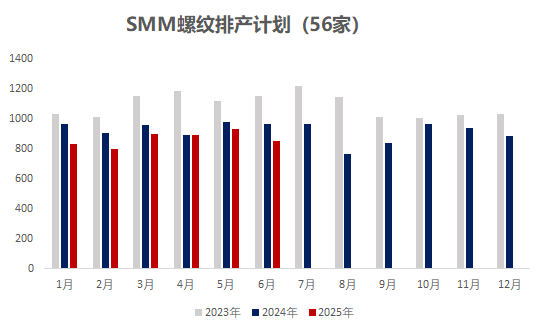

Since April 2022, the SMM rebar production schedule sample has been expanded to include 56 enterprises.

According to the SMM survey data from 56 key steel-producing enterprises:

- The planned rebar production for June was 8.5197 million mt, a decrease of 820,600 mt from the actual production in May, representing an 8.79% decline MoM;

- The planned wire rod production for June was 3.4809 million mt, a decrease of 208,500 mt from the actual production in May, representing a 5.65% decline MoM.

Chart-1: Rebar & Wire Rod Production Schedule of Major Construction Steel Mills (56 Enterprises)

Source: SMM

Overall:

In May, the national construction steel prices fluctuated downward. In the first ten days, the temporary suspension of overseas tariff hikes led to a phased rebound in spot prices. However, in the middle and latter parts of the month, the macro real estate data performed poorly, and there were no significant improvements in other news, with demand gradually transitioning towards off-season expectations, and spot prices continued to decline. On the cost side, iron ore prices remained relatively firm, while coking coal and coke continued to offer concessions. There was an expectation of a fourth round of coke price cuts, and most steel mills still had profit margins, with overall benefits basically ranging between (-200-200) yuan/mt.In June, steel mill maintenance, combined with a shift in product mix,led to the highest annual reduction in rebar production.Specifically, the construction steel production schedule in North and Central-South China slightly increased, mainly due to the planned blast furnace resumptions in steel mills in June, with synchronous increases in construction steel rolling lines. In contrast, multiple steel mills in East China shifted to producing billets, round steel, and other products. Additionally, individual steel mills were affected by production restrictions, with blast furnaces scheduled for shutdown, leading to a significant overall reduction. In North-West China, a steel mill halted blast furnace production in early June due to cash flow losses, while in South-West China, a steel mill experienced difficulties in pig iron tapping, both affecting overall construction steel production.

By region:

Table-1: Actual Rebar and Coiled Rebar Production in May vs. Planned Production in June

Source: SMM

In North-East China, steel mill profits ranged between (-100-100) yuan/mt. Some steel mills resumed blast furnace production, but pig iron was redirected towards HRC production, while other steel mills generally maintained previous production levels, with minimal overall changes.

In North China, steel mill profits ranged between (-200-200) yuan/mt. Recently, profit margins among steel mills in the region continued to diverge, with most steel mills achieving comprehensive profits of 100-200 yuan/mt, though some incurred losses of around 200 yuan/mt. Despite some steel mills scheduling blast furnace maintenance in June, others indicated that with profits, they planned to slightly increase construction steel production. Based on comprehensive data, production in North China slightly increased MoM in June.

In East China, steel mill profits ranged between (0-300) yuan/mt. Currently, steel mills in the region achieve better benefits from producing construction steel compared to other regions. However, planned production reductions in June were more pronounced, influenced by policies to reduce crude steel output, with some steel mills planning to halt blast furnaces and rolling lines. Additionally, due to strong order books for billets and special steel in the earlier period, which are still in the concentrated delivery phase, the reduction in construction steel production was relatively significant.

In north-west China, steel mill profits ranged from (-200-50). Some steel mills producing construction materials were already experiencing negative cash flow, so they arranged blast furnace maintenance in late May and early June, and simultaneously halted 1-2 construction material rolling lines, leading to a continued decline in overall production.

In central and south China, steel mill profits ranged from (-100-100). Some steel mills in the region had production resumption plans for construction material rolling lines in June, with a significant rebound in overall production. Other steel mills, although profitable, basically maintained production, with relatively small changes in output.

In south-west China, steel mill profits ranged from (-200-100). Some individual steel mills faced production disruptions in blast furnaces, and planned to halve their production of finished products in June.

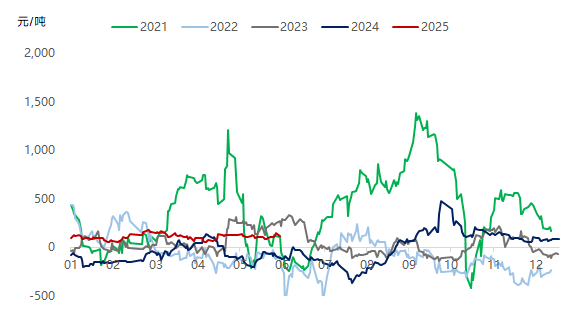

Chart-2: Trend of real-time profits for rebar production by steel mills from 2020 to present

Data source: SMM

Chart-3: Marginal profit situation for rebar in early June at sample steel mills

Data source: SMM

Looking ahead, influenced by the news of crude steel production cuts and the transition into the off-season for demand, some individual steel mills have successively arranged production cut plans. Secondly, with the delivery of billet orders for external sales in east China and the good order-taking and profitability of round steel, special steel, and other varieties at multiple steel mills, steel mills are diverting pig iron from the construction materials sector to other varieties, resulting in a significant reduction in overall construction material production by steel mills in June. Losses at EAF steel mills have intensified, with some steel mills planning to halt operations, and production is expected to continue to decline in the future. On the demand side, affected by high temperatures in the north and plum rain season in the south in June, construction site progress is limited, and the downstream procurement pace will slow down, with demand continuing to deteriorate compared to May. On the whole, there is an expectation for further concessions on the raw material side, and steel mill profits will be maintained in the short term. However, considering the pressure of inventory accumulation in steel mills during the off-season, manufacturers will adjust their production structures accordingly or arrange annual maintenance plans in advance. Under the situation of a decline in both supply and demand, it is expected that the spot market trend for construction steel in June may continue to be in the doldrums, but the fluctuation range will narrow compared to May.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)